Facebook

Facebook Whatsapp

Whatsapp LinkedIn

LinkedIn Pinterest

PinterestEmbedded Finance: A complete guide

Table of Contents

- Introduction

- Understanding Embedded Finance: The Foundation

- Key Components of Embedded Financial Services

- Real-World Use Cases Driving Business Growth

- The Business Impact of Embedded Fintech

- Best Practices to Follow While Enabling Embedded Finance

- Technology Infrastructure for Embedded Finance Implementation

- Regulatory Considerations and Risk Management

- Future Trends in Embedded Financial Services

- Getting Started with Embedded Finance

- Frequently Asked Questions

As finance evolves rapidly, embedded finance is transforming the way services are offered across various industries. For startups and established businesses alike, understanding embedded finance has become crucial for staying competitive and meeting customer expectations in today’s digital economy.

Embedded finance involves effortlessly weaving financial functionalities into apps, platforms, or user journeys that aren’t primarily financial. Instead of redirecting users to separate banking or payment platforms, businesses can now offer financial services as a natural part of their core product offering.

Understanding Embedded Finance: The Foundation

At its core, embedded finance eliminates the friction between commerce and financial transactions. When you order a ride through Uber and pay automatically through the app, or when Amazon offers instant financing for large purchases, you’re experiencing embedded finance in action.

This integration goes beyond simple payments. Embedded financing encompasses lending, insurance, banking services, investment options, and more, all delivered within the context of the primary business relationship. The goal is to make financial services invisible yet accessible, creating a seamless user experience that drives engagement and revenue.

Market Growth Insight

According to McKinsey, embedded finance is reshaping the modern financial system at a fast pace. In Europe alone, revenues from embedded finance are expected to surpass €100 billion by 2030, accounting for as much as 10–15% of banking revenue pools. The share of retail and SME lending initiated through embedded finance channels is expected to rise from 5–10% today to 20–25% by the end of the decade, underscoring the sector’s rapid growth and increasing adoption.

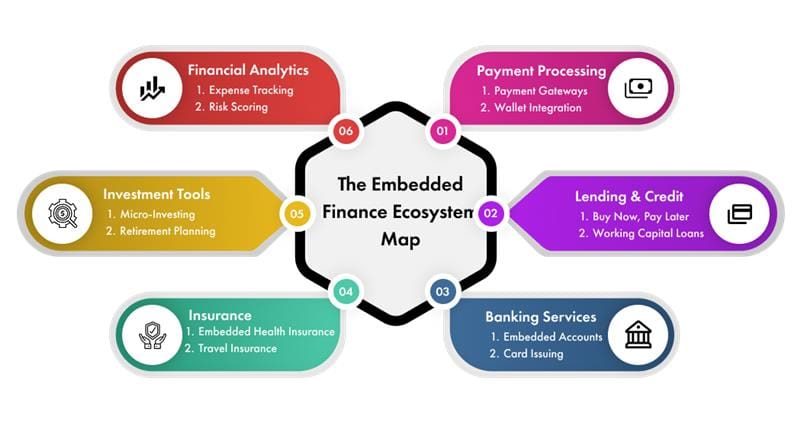

Key Components of Embedded Financial Services

Embedded financial services encompass several key areas that businesses can integrate into their platforms:

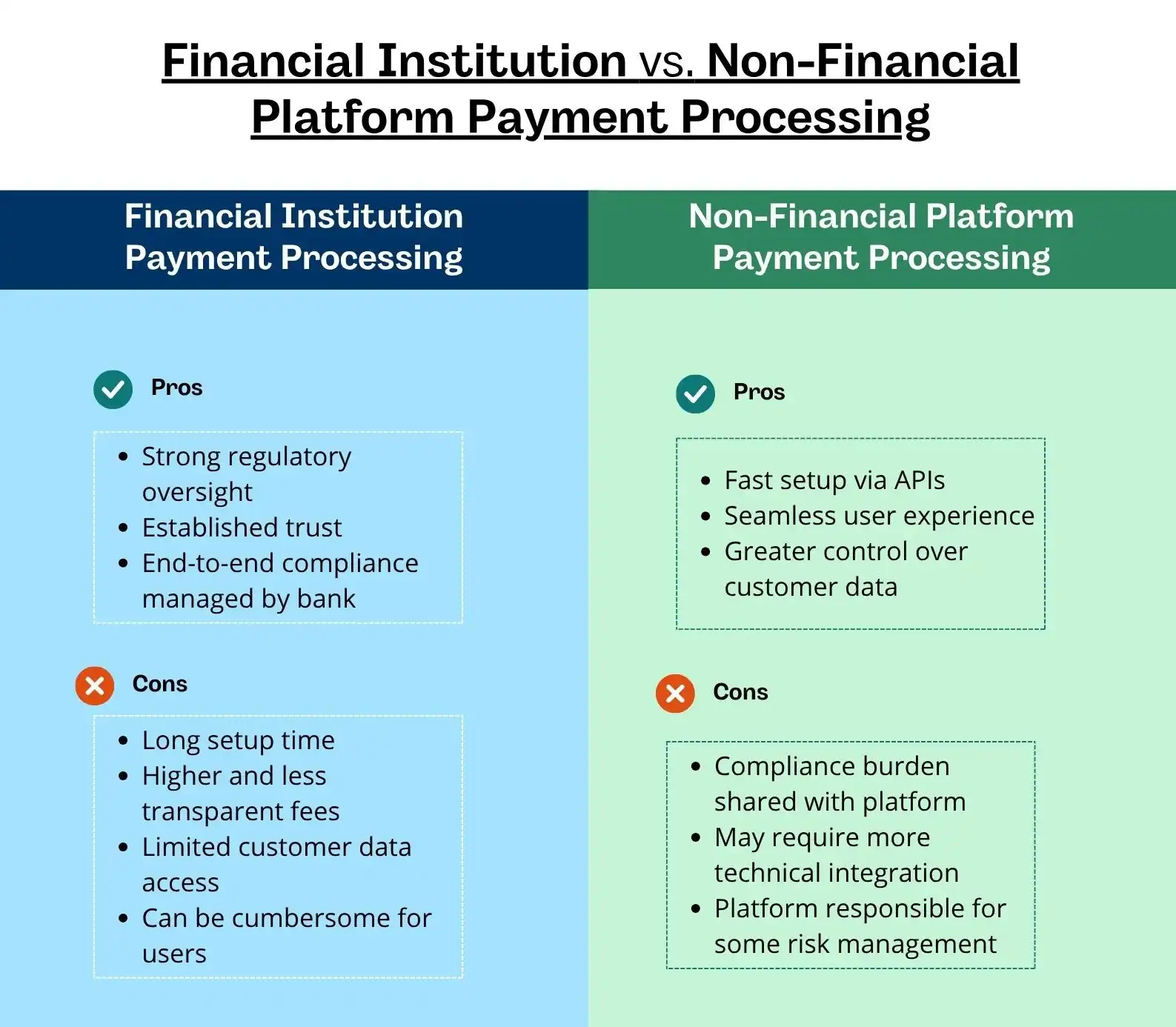

- Payment Processing forms the foundation, enabling businesses to accept payments without redirecting customers to external payment gateways. This leads to a more seamless checkout process and helps minimize abandoned shopping carts.

- Lending and Credit Services are incorporated into platforms that can instantly provide customers with financing solutions. Buy Now, Pay Later (BNPL) solutions have become particularly popular, with companies like Klarna and Afterpay demonstrating how embedded finance can boost conversion rates by 20-30%. E-commerce sites can integrate BNPL directly at checkout, while B2B platforms can offer working capital loans to their merchant partners.

- Banking Services include features like digital wallets, account management, and money transfers. Gig economy platforms often provide instant pay features, allowing workers to access earnings immediately rather than waiting for traditional pay cycles.

- Insurance Products can be embedded to provide protection relevant to the platform’s use case. Travel booking sites offer travel insurance, while rental platforms provide property damage protection.

Real-World Use Cases Driving Business Growth

The versatility of embedded finance creates opportunities across virtually every industry. Understanding these use cases helps businesses identify where embedded finance can add value to their operations.

- E-commerce Platforms use embedded finance to offer multiple payment options, instant checkout experiences, and flexible financing. Companies like Shopify provide merchants with integrated payment processing, lending services, and business banking features, while retailers increasingly offer BNPL options that can increase average order values by 30-50%. This creates a comprehensive commerce ecosystem that benefits both merchants and consumers.

- Gig Economy Applications leverage embedded financial services to provide instant payouts, expense management, and financial planning tools. DoorDash drivers can access their earnings immediately, while Uber includes debit cards and spending insights to help drivers manage their finances.

- B2B Marketplaces integrate embedded financing to help small businesses access working capital, manage cash flow, and streamline payments. These platforms can offer invoice factoring, equipment financing, and supplier payment solutions.

- Software-as-a-service (SaaS) Companies embed financial services to expand their value proposition. Accounting software might offer integrated lending, while project management tools could provide expense tracking and reimbursement features.

This trend is reflected in Deloitte’s latest industry outlook, which shows that US banks are increasingly turning to noninterest income – such as payments, lending, and financial services embedded in digital platforms – to sustain growth as traditional revenue streams face pressure.

As banks and platforms diversify their offerings, embedded finance is becoming a critical lever for driving business value across industries.

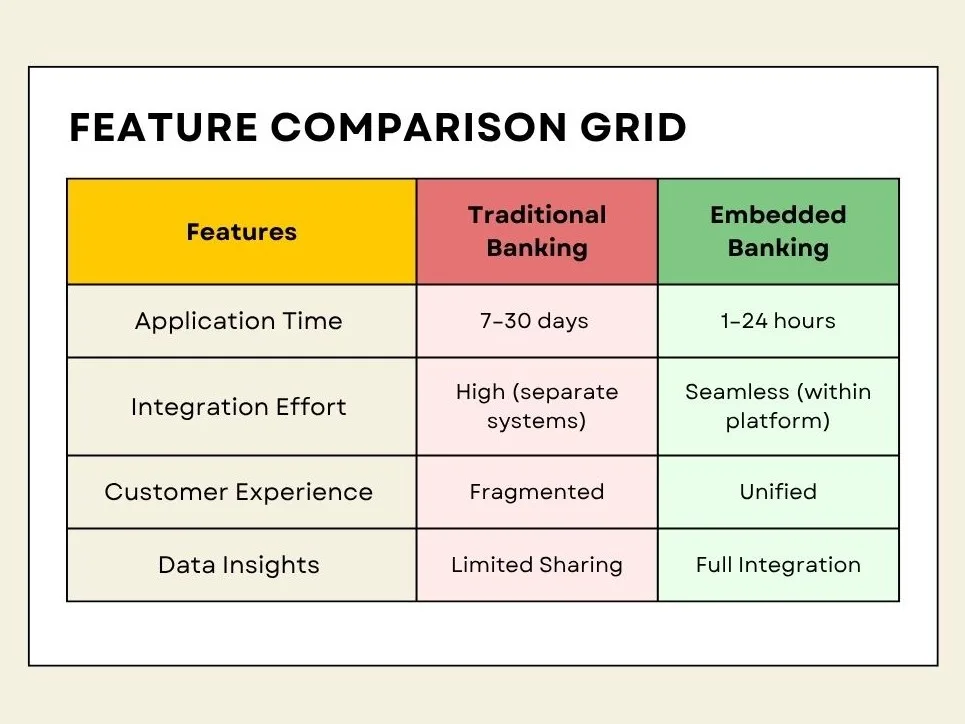

Traditional vs. Embedded Lending Solutions

| Metric | Traditional Lending | Embedded Lending |

| Application Time | Days to weeks: in-person visits, paperwork | Minutes to hours; fully digital, in-app |

| Approval Rates | Lower; strict criteria, manual review | Higher; flexible criteria, automated checks |

| Integration Complexity | High manual processes, siloed systems | Low; API-driven, seamless with platform |

| Customer Experience | Cumbersome, slow, requires branch visits | Frictionless, instant, stays on the platform |

| Cost Structure | Higher costs (manual labor, acquisition) | Lower costs (automation, digital onboarding) |

The Business Impact of Embedded Fintech

Implementing embedded fintech solutions delivers measurable benefits that directly impact business growth and customer satisfaction. Companies typically see increased customer retention, higher transaction volumes, and new revenue streams.

According to Boston Consulting Group, financial institutions with mature embedded analytics capabilities report operational cost reductions of 15–25%, significant improvements in customer experience (NPS up by 25 points), and notable gains in efficiency and risk management.

- Revenue Diversification is a key benefit lies streams through new financial service offerings. By offering financial services, businesses can earn additional income through interchange fees, lending margins, and service charges. This creates multiple revenue streams beyond the core product offering.

- Customer Stickiness improves dramatically when financial services are embedded within the platform. Customers become more engaged and less likely to switch to competitors when their financial needs are met within the existing ecosystem.

- Operational Efficiency increases as embedded finance reduces the complexity of managing multiple vendor relationships. Companies can enhance operational efficiency and elevate customer service by embedding financial capabilities into their ecosystems.

- Data-driven insights become more valuable when financial transaction data is combined with business intelligence. This view makes a better way to make decision-making, risk assessment, and personalized service delivery.

Best Practices to Follow While Enabling Embedded Finance

Successfully implementing embedded finance requires careful planning and adherence to industry best practices. These guidelines help ensure smooth deployment and optimal results.

- Start with Customer Needs Assessment. Before integrating any financial services, thoroughly understand your customers’ pain points and economic challenges. Survey users, analyze support tickets, and identify where financial friction occurs in their journey with your platform.

- Choose the Right Technology Partners. Select fintech partners and APIs that align with your technical capabilities and business objectives. Evaluate factors like integration complexity, scalability, compliance support, and fee structures. Ensure your chosen partners can grow with your business.

- Prioritize Security and Compliance. Financial services integration introduces additional regulatory requirements and security considerations. Implement robust authentication, encryption, and monitoring systems. Keep up with regulations such as PCI DSS, KYC, and AML to ensure compliance and build trust in your financial solutions.

- Design for Seamless User Experience. The embedded financial service should feel natural within your existing platform. Avoid jarring design changes or complex workflows that disrupt the user experience. Test thorough user testing before launching to ensure a smooth and effective rollout.

- Implement Gradual Rollout Strategies. Start with core financial services that address the most pressing customer needs. Gradually expand your offerings based on user adoption and feedback. This approach reduces risk and allows for iterative improvement.

- Monitor Performance Metrics. Track key indicators like adoption rates, transaction volumes, customer satisfaction scores, and revenue impact. Use this data to optimize your embedded finance offerings and identify expansion opportunities.

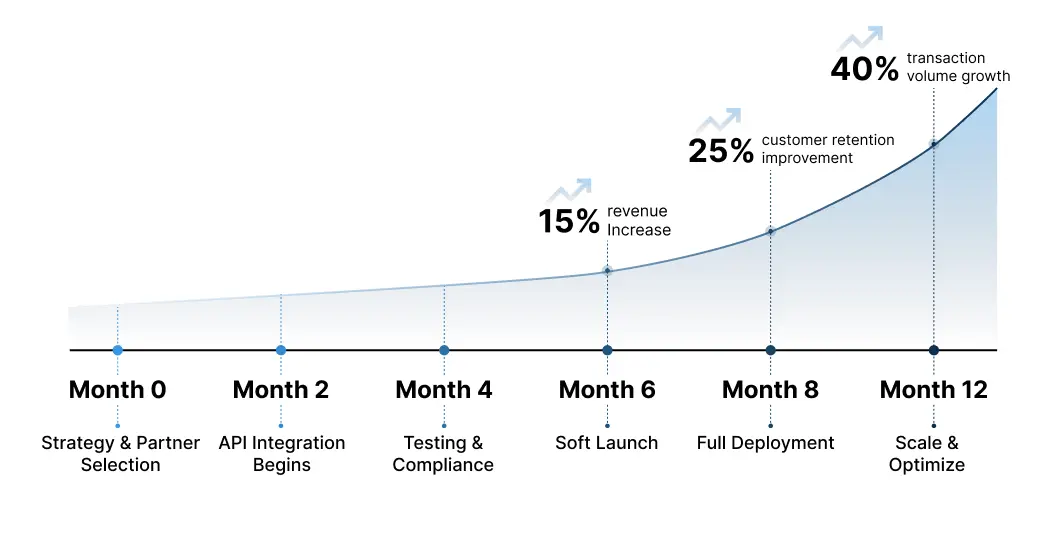

While specific implementation timelines vary by complexity, industry research from Forrester suggests that simple embedded payment integrations can be completed in as little as 3–6 months, while more complex solutions such as embedded lending or insurance may require 9–18 months for full deployment. Success rates are highest for organizations that follow a phased rollout, prioritize customer needs, and select experienced technology partners.

Technology Infrastructure for Embedded Finance Implementation

Building embedded finance capabilities requires robust technology infrastructure that can handle financial transactions securely and efficiently. The foundation typically includes API integrations, compliance management systems, and user interface components.

- API-First Architecture enables flexible integration with multiple financial service providers. This approach allows businesses to mix and match services from different providers while maintaining a consistent user experience.

- Microservices Design supports scalability and maintainability. Each financial service can be developed, deployed, and updated independently, reducing system complexity and improving reliability.

- Real-Time Processing Capabilities ensure that financial transactions occur instantly, meeting user expectations for immediate service. This includes payment processing, account updates, and notification systems.

Regulatory Considerations and Risk Management

Embedded finance implementation must address various regulatory requirements and risk factors. Understanding these considerations helps businesses prepare for compliance obligations and operational challenges.

- Licensing Requirements may apply depending on the financial services offered and the jurisdiction served. Some embedded finance models require specific licenses, while others can operate under partner licenses.

- Data Privacy Compliance becomes more complex when handling financial information. Businesses must ensure compliance with regulations like GDPR, CCPA, and financial privacy laws.

- Risk Assessment and Monitoring systems help identify and mitigate potential fraud, credit risks, and operational issues. Implementing comprehensive monitoring from the start prevents problems and ensures sustainable growth.

Future Trends in Embedded Financial Services

The embedded finance market continues to evolve rapidly, with new technologies and use cases emerging regularly. Knowing these trends helps businesses get ready for future opportunities and potential hurdles.

- Artificial Intelligence and Machine Learning enhance embedded finance through improved risk assessment, personalized financial products, and fraud detection. These technologies enable more sophisticated financial services within embedded platforms.

- Blockchain and Cryptocurrency Integration are creating new possibilities for embedded finance, including decentralized finance (DeFi) features and digital asset management.

- Industry-specific solutions are becoming more common as embedded finance matures. Vertical-specific financial services address unique industry needs more effectively than generic solutions.

Getting Started with Embedded Finance

For businesses ready to explore embedded finance opportunities, the journey begins with strategic planning and partner selection. Start by identifying the specific financial pain points of your customer’s experience and evaluating how embedded solutions could address these challenges.

Partner with an experienced Fintech software development company that understands both the technical and regulatory aspects of embedded finance implementation. The right technology partner can accelerate your time to market while ensuring compliance and security.

At Fortunesoft IT Innovations, we specialize in helping businesses implement embedded finance solutions that drive growth and improve customer experience. We navigate the complexities of finance integration and support you through each stage of implementation.

Ready to transform your business with embedded finance? Contact our expert development team to discuss your embedded finance implementation strategy.

Frequently Asked Questions

- What is the difference between embedded finance and traditional fintech?

Embedded finance integrates financial services directly into non-financial platforms, while traditional fintech operates as a standalone financial service provider. Embedded finance creates seamless experiences within existing customer journeys.

- How long does it take to implement embedded finance solutions?

Implementation timelines vary based on complexity and scope, typically ranging from 3 to 12 months. Simple payment integration might take a few weeks, while comprehensive financial service suits require more extended development periods.

- What are the key regulatory hurdles faced by embedded finance?

Key challenges include compliance with financial regulations, data privacy laws, and licensing requirements. BNPL services, for example, are facing increased regulatory scrutiny regarding consumer protection. Working with experienced partners helps us navigate these complexities effectively.

- What are the most popular embedded finance services?

The most popular embedded finance services include payment processing, Buy Now Pay Later (BNPL) solutions, digital wallets, instant lending, and business banking services. BNPL has seen explosive growth, with the market expected to reach $95 billion by 2026.

- Can small businesses benefit from embedded finance?

Yes, embedded finance solutions are scalable and can benefit businesses of all sizes. Many API-based solutions offer flexible pricing models that work for smaller operations, and BNPL integration can be particularly beneficial for small e-commerce businesses looking to increase sales.

- What security measures are required for embedded finance?

Essential security measures include encryption, secure authentication, PCI compliance, fraud monitoring, and regular security audits. These obligations differ depending on the type of financial service being provided.

Author Bio

Related Blog

12 min read

Start Chat

Start Chat