The impact of COVID-19 on traditional banking models is quite emphatic. The pandemic has profoundly affected consumer demands. The technology facilitating these demands are rapidly evolving for financial services.

Non-financial companies have redoubled their efforts and optimized their methodologies to offer products and services to their customers that would solve specific needs. This introduced an extraordinary potential for both fintech companies and non-financial institutions to offer highly targeted integrations with the help of BaaS.

Today, embedded finance is set to attract millions of customers by significantly promoting the democratization of finance. A recent study by Lightyear Capital states that embedded finance will grow up to $230 billion by 2025, creating a value of more than $1 trillion and is predicted to rise to $3.6 trillion by 2030. Moreover, embedded finance offers a full suite of enterprise digital solutions right from wealth management to global payment platforms, seamlessly integrated into other services and sectors.

Embedded finance brings a lot of innovative opportunities in areas such as specialized SaaS, marketplaces, eCommerce, mobility or telcos for a wide range of business verticals. These aren’t limited to industry giants, but also offer tremendous business opportunities for local SaaS businesses by seamless embedding of financial services with the help of BaaS providers.

Let’s check out how this growing integration of tech and financial services reshapes the financial ecosystem.

Some facts and figures

According to the research by Lightyear Capital,

(A) The four dominant areas that are predominantly focused on embedded finance in 2021:

1. Consumer Lending

2. Insurance

3. Wealth Management

4. Payments

(B) These key areas are predicted to be responsible for $2.6 billion in revenue for wealth management

(C) The compound annual growth rate (CAGR) is predicted to be 62% i.e. from $1.7 billion to $15.7 billion for consumer lending

(D) The CAGR is predicted to be increasing by 62% for Insurance from $5 billion to $70.7 billion

(E) Payments are forecasted to see a whopping increase at the rate of 54% from $16.1 billion to $140.8 billion

What is driving the growth of Embedded Finance?

The major reasons behind the rise of embedded finance are:

1. Consumer buying behaviors: With the emergence of digitization, there has been a shift in the consumer buying behaviors and patterns. This unfolded the digital platform economy driving a consumer-led trend that changed the purchase habits for most adult generations and a new norm for the younger ones. Some of the leading names are Amazon, Facebook, Uber, and so on and henceforth.

2. Willingness to adapt: There are many consumers who are willing to avail financial services from a non-traditional financial provider. According to a research by Cornerstone Advisors, 46% of the Millennials between the age 26-40 years show interest and check accounts with Amazon if they provide any kind of financial service to them.

3. Openness to share personal data: It is observed that there is a lot of willingness among the younger generation to share personal data. Embedded Finance has the potential to provide personalized customer experience with the help of the data it gets from the customers.

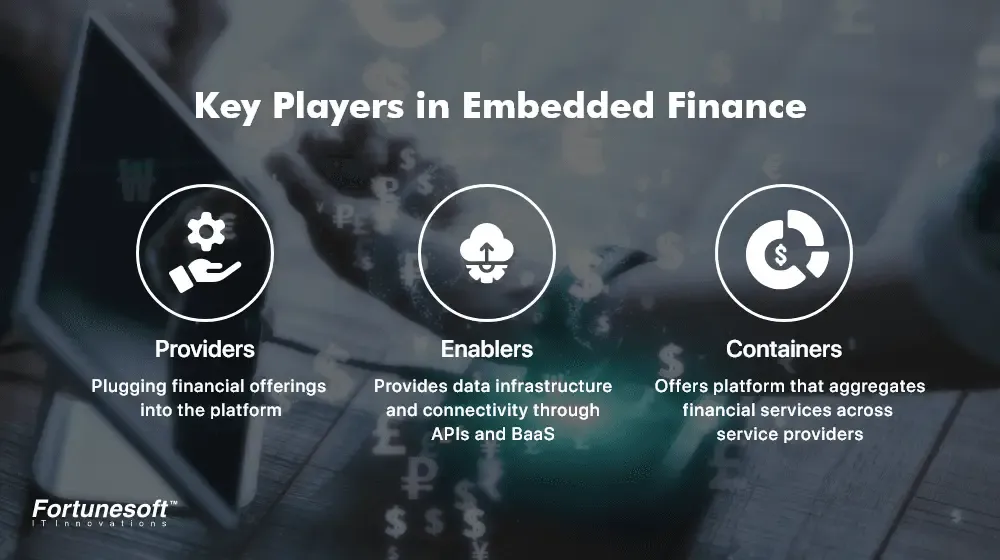

Main players in the embedded finance

The tech companies that are driving the growth of embedded finance can be categorized as:

- Providers: These are the service providers that plug financial offerings into platforms. A service provider provides IT solutions and services to end-users or organizations. These service providers are typically fintech development companies that offer an exquisite suite of fintech development services and digital solutions tailored to your business requirements. They do this to increase distribution and improve customer retention. The fintech services they provide are pay per use, hybrid, and on-demand services.

- Enablers: These are the organizations that provide data infrastructure and connectivity through APIs and banking-as-a-service(BaaS) platforms. Enablers are those organizations that facilitate or enhance an existing solution with the help of technologies and frameworks. The Banking as a Service(BaaS) players rent out their core banking infrastructure to power numerous fintech applications and services.

- Containers: This category of organizations offer platforms that aggregate financial services across providers. This allows the customers to access a wide range of solutions in a frictionless manner. Consumers want to access financial services through web, mobile, POS, and others. Organizations create a link between the banks and consumers’ data and provide a platform to allow consumers to access end-to-end financial services.

Benefits of Embedded Finance

Why is embedded finance worth your attention? Here are the top 5 reasons!

- Convenience: Fintech mobile app development companies are striving hard to simplify customer processes for large to small enterprises by adding banking capabilities with the help of BaaS service providers

- Frictionless payments: Crafting seamless experience through embedded financial services in non-finance apps like QR code, BNPL, digital wallets, and rideshare insurance

- User-experience: Fintech software developers have expertise in developing a user-friendly interface that engages a user with their fintech product

- Conversions: Better understanding to serve customers due to greater visibility and convenience

- Revenue: Increase in revenue by 5X times per user through integrating financial services into the company’s current offerings

Applications of Embedded Finance

All these years, financial services have integrated into multiple software and applications offered by non-financial providers with the help of fintech development companies. This trend of embedded finance has become disruptive in payments, banking, and technology today as it has showcased a tremendous potential in reshaping financial services for enterprises and consumers. As embedded finance has become a tech stack and a part of their fintech software development services for companies of all sizes, they are finding their position in the following applications:

1. PoS, eCommerce, & vertical software vendors: Embedded finance offers integrated payment and lending services to their sub-merchants such as Shopify, Toast, Lightspeed, and so on. Sub-merchants are merchants that process transactions under a merchant aggregator.

2. Ridesharing: Ridesharing companies like Uber offers various financial services such as digital wallets, insurance, instant payouts, debit cards to both the rider and the driver.

3. Consumer-focused fintech apps: Fintech apps and software solutions that are focused on consumers’ specific needs and expand their app’s functionalities to meet these demands through debit cards, loan installments, instant lending, immediate loan disbursement, and so on. Some popular examples of consumer-focused fintech apps are Revolut, Klarna, Square.

4. Consumer tech companies: Large tech giants such as Apple, Google, Facebook, Amazon, Telcos offer digital wallets, P2P payment services, credit and lending services, debit cards to their end-users.

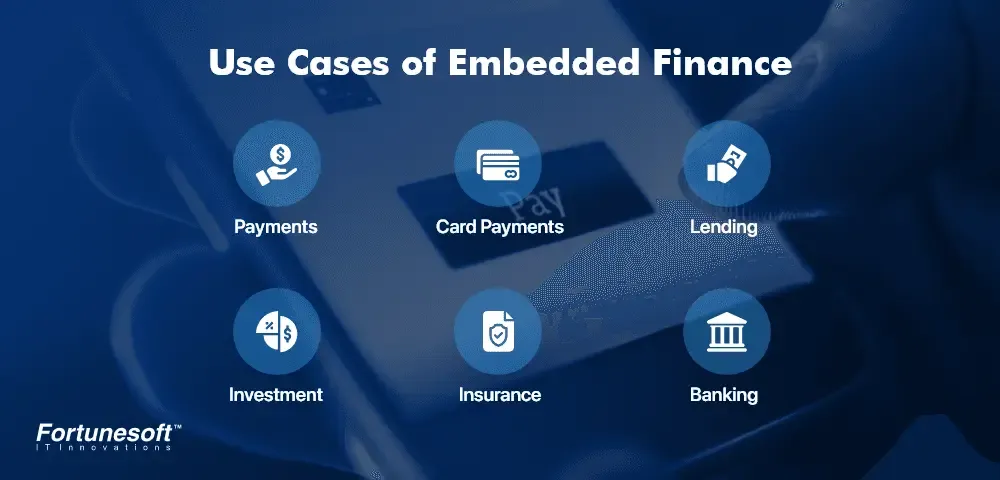

Use Cases of Embedded Finance

With embedded finance, you can bridge the gap between consumers and companies. Check out some of the use cases of embedded finance and find out where you can fit it in.

1. Payments

Imagine a situation where you are using public transport for your commute and you run out of cash. In this situation, embedded payments come for your rescue. Ride-sharing apps like Uber include embedded payments that free you from handling cash. You can simply pay using the app once the ride is over.

Another popular example is the famous coffee chain Starbucks where you use embedded payments. Their app allows you to order and pay as well. Also, the Starbuck app rewards them with points that can be redeemed as per T&C for future purchases.

2. Card Payments

If you want to streamline payments and simplify the process of paying employees or contractors, own a branded credit card. You can cut using cheques and issuing direct deposits by delivering payments to your own credit cards. You can deal with the card-issuer that in exchange for a white-label debit card, you will pay some interchange fees.

One of the popular examples is PayPal where users can link their PayPal account to their bank account. Also, PayPal allows users to apply for the company’s cash card. This provides users with direct access to their PayPal accounts where the user can use it immediately or use it in ATMs instead of waiting for a day or two.

3. Lending

Do you remember the last time you borrowed money, what did you do? You might have applied for a loan or a credit card. With embedded banking, lending is hassle-free. With apps like Klarna and AfterPay, you can immediately avail of loans at the point of purchase. These apps allow consumers to avail of monthly installments as well for purchase.

4. Investments

One of the popular examples of embedded investment is Acorns. An Acorns user gets a seamless and touchless investment experience. The user is free from memorizing money transfers. Also, their portfolio is adjusted as per the market changes automatically. This helps Acorns users to relax from paying attention to the values of stocks or mutual funds. Acorns help people invest their spare change by rounding up purchases.

5. Insurance

With embedded insurance, the insurance agent and broker gets eliminated. Thus, purchasing an insurance policy becomes quite easy.

Buying insurance is a vital part when you purchase a car or home. Also, insurance is still now considered a separately entire process. Therefore, to speed up the entire process and at the same time increase the bottom lines, some organizations are trying to embed insurance in their process while making a major purchase.

One such popular example is Tesla where it offers an insurance program and lets people choose the appropriate coverage instantly with much less cost.

6. Banking

Embedded banking is another buzzword that offers banking services to customers. With embedded banking, organizations can eliminate the use of making a separate bank account in financial institutions. For example, Shopify offers embedded banking to businesses where they allow them to set up accounts for their companies with Shopify.

A major challenge that is still a concern in Embedded Finance

Though the benefits that embedded finance has for you is undeniable, you still have to combat some obstacles. One of the major drawbacks of embedded finance is its widespread acceptance.

Fintech companies that want to stay ahead in the competitive curve find various innovative ways to reduce customer friction as much as possible. Therefore, they try to incorporate embedded technologies wherever possible into their fintech applications to provide their consumers an optimal user experience.

Adopting embedded finance opens up a wide array of revenue sources by reinventing the traditional services that they deliver to their clients. This welcomes convenience for both companies and consumers. Thus, embedded finance will contribute to the economy at large, particularly for the fintech industry.

Today digitalization is flourishing across various traditional industries. It is creating a whole lot of opportunities around the globe for revolutionizing financial services in non-fintech businesses through embedded finance. We hope that the post-COVID economy brings in various events that boost this pattern of embedded finance to get repeated in environments around the globe to unbundle financial processes.

In a nutshell

Embedded finance has become an act of assertive creativity powered by technology. Fintech app development companies around the globe are trying hard to leverage the benefits of embedded finance to create new opportunities in businesses, optimal experiences, platforms, and products.

Undoubtedly, embedded finance is the future of financial services as there are a lot of use cases that trigger its potential even more in the finance ecosystem. 2021 is all about how fintech application development companies are focusing on specific segments where the above-defined use cases will perfectly fit in. BaaS providers will play a major role to develop new products that will help your business to achieve bigger in specific niches.

Embedded finance will prove to be a key milestone in the fintech revolution in 2021 with its tremendous potential to change the face of financial services.