Open Banking is a revolutionary technology in the digital world that forces banks to reinvent their traditional business models. Banks leverage open banking to collaborate and partner with fintech and third-party providers to stay ahead of this competitive curve. This rapidly evolving ecosystem is highly driven by Open Banking API as it changes the way incumbents interact with third-party providers. Open Banking not only transforms this but also revamps the way a consumer interacts with them.

Let’s explore more about open banking API and how leveraging open banking API will create an impact on banks and its customers.

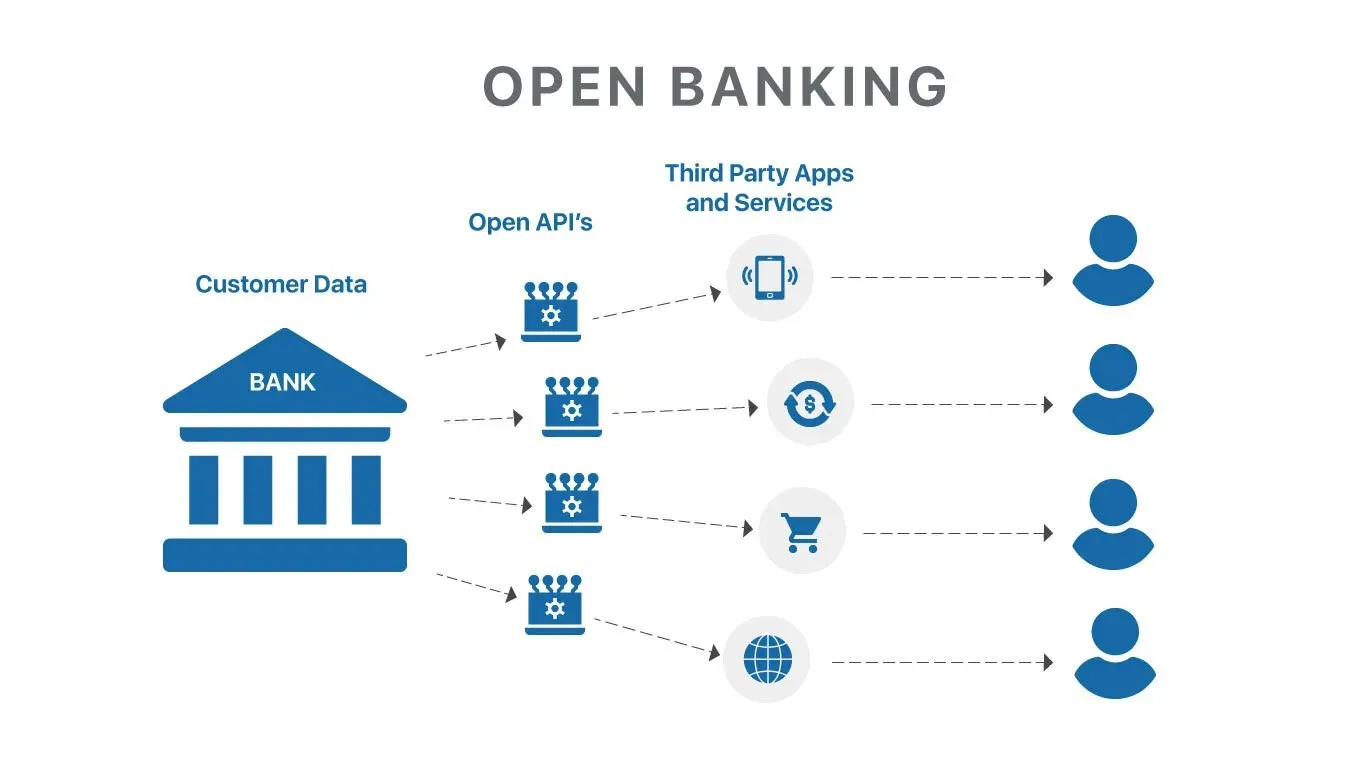

What is Open Banking API and How It Connects to Open Finance API?

Open Banking enables sharing of customer’s financial information securely with the customer’s approval.

API permits third-party providers like Fintech to access the customer’s financial information that, in turn, helps to craft fintech apps and services for enhanced digital experiences. The fintech products that are built are not only for customers but also, for SMEs and startups to boost growth and revenue.

As open banking enables sharing of information to a regulated third-party provider, for your consent for sharing the information, you need to use your online banking credentials to log into your account and approve the third-party to access the information. The login credentials are always handled by the customer’s bank and not the TPP. Moreover, when the customer approves to access his information, TPPs have only “read-only” access, and therefore, TPPs can’t carry out a transaction.

Key Benefits of Open Banking APIs and Banking-as-a-Service Solutions

Open banking helps banks to enable higher customer engagement. Moreover, open banking API offers new insights that helps businesses and customers to make decisions about their financial assets. Let’s checkout the top benefits of Open Banking API.

- Customer Engagement: Enables customers to engage with their financial data in a secure, agile, and future-proof method with the changing financial ecosystem and customer demands.

- Payments: Boosts digital revenue by allowing customers to pay through digital and mobile wallets via their smartphones for almost every purpose

- Banking-as-a-Service (BaaS): API-led connectivity ensures speed, agility, and innovation for launching new financial products.

- Remittance & Currency Exchange: Supports international money transfers and remittances through a simple, faster, and less expensive process with Open Banking API

- Customized Product Offerings: Benefits customers immensely by allowing financial firms to offer personalized products and services with greater transparency.

Best Practices for Implementing Open Banking API

When implementing Open Banking API, banks, fintech, and regulators should focus on:

1. Time frame:

You can’t have an aggressive schedule to implement transformational modifications to complex financial systems. A financial system includes a lot of stakeholders. Therefore, you should have a flexible and properly planned time frame that will help in coordinating and implementing all the tasks and elements in a hassle-free manner.

2. Smooth interaction and cooperation of open platforms

The financial ecosystem has already owned a plethora of APIs and world-class solutions that have delivered amazing customer experiences. To gain a frictionless adoption of open architectures, you need to accept open technologies to better flourish.

3. Flexibility

Today, the pandemic has resulted in the revamping of financial models. Financial solutions that offer limited offerings are outdated. Consumers need personalized services. To plug in these new services in your fintech apps, you need to choose the best technological framework that can quickly adapt to the changes and also abide by the regulations.

4. Preach the public

If you’re planning to make a significant change in banking services, your consumers have the right to know about those modifications and require knowledge to become aware of those services. Offer consumers the time to get acquainted with these changes and leverage the benefits of the same for higher engagement.

Top use cases of Open Banking

Open banking has gained huge popularity and has amplified due to the global pandemic and the surge in demand for online services. As of March 2025, 1 in 5 digitally active UK consumers and small businesses are using Open Banking APIs, up from just 1 in 17 in March 2021, marking a clear upward trajectory in adoption.

Open Banking API is gaining popularity, especially post-pandemic, as digital financial services grow. Use cases include:

- KYC process automation: Open banking offers a streamlined process to fetch and verify customer information necessary for the customer due to diligence procedures.

- Customer onboarding: Open banking offers a simplified customer onboarding process by fetching hard-to-access financial information seamlessly. The customer onboarding process involves account and identity verification, auto-filling forms, income verification, and affordability checks.

- Financial management: Open banking API offers an optimal digital customer experience by allowing aggregation of financial information from different accounts and banks for easy money management. Moreover, open banking API allows easy finance management by offering finance dashboards, auto-saving, and smart budgeting. Also, open banking APIs play a major role in managing SME finances by offering seamless account aggregation, automated accounting, and affordability checks.

- Transaction monitoring: Open banking offers enhanced methodologies to improve customer profiles and make it easier for abnormal activity identification or any kind of anomalies in the data.

- Insurance: Open banking API offers unparalleled visibility of customers’ spending behaviors that results in better decisions for lending and insurance.

- Payments: Open banking allows a direct account to account payments, eliminating costs incurred by card processors. It further allows the customer to carry out the transaction from a single place.

- Product comparisons: Open banking platforms and advanced data analytics offers product recommendation service to the customer based on their spending behavior.

Top Open Banking API Trends in 2026

Customer demand for faster, cheaper, and safer digital finance is pushing account-to-account (A2A) payments and data-sharing into the mainstream. In the UK alone, 13.3 million consumers and SMEs now actively use Open Banking, with 31 million Open Banking payments in March 2025, about 8% of all Faster Payments, and payments volume growing ~70% year over year.

1. Using Open Banking APIs for A2A Payments

Account-to-Account (A2A) payments are becoming a core use case for Open Banking. According to Open Banking data, merchants, government agencies, and investment platforms increasingly offer “Pay by Bank” for instant checkout, bill payments, and top-ups. The shift is driven by lower costs compared to cards, strong customer authentication (SCA), and faster settlement. In the UK alone, monthly Open Banking payments have reached ~31 million, marking a tipping point for A2A adoption.

2. Variable Recurring Payments (VRP) expand beyond sweeping

According to Open Baking, VRP now makes up ~13% of Open Banking payments. Regulators and industry are moving toward commercial VRP (cVRP) for limited, low-risk use cases (e.g., utilities, government, regulated financial services) in H2 2025, backed by an industry initiative to stand up the commercial model.

3. Standards & governance level up (UK Future Entity)

The UK’s Joint Regulatory Oversight Committee (JROC) has set out the design for a new Future Entity to maintain common API standards, monitor performance, and ensure interoperability, key to scaling reliable Open Banking payments and data services. The FCA’s FS25/4 feedback statement (Aug 2025) details this design.

4. From Open Banking to Open Finance

Europe is moving beyond current accounts with the proposed Financial Data Access (FIDA) regulation, expected to be adopted in 2025. FIDA widens secure data-sharing across savings, investments, insurance and more, unlocking broader “Open Finance” API use cases.

5. The US formalizes (but refines) its Open Banking rule

The CFPB’s final Personal Financial Data Rights rule (Section 1033) was issued in Oct 2024, with phased compliance beginning April 2026 for large firms. In July 2025, the CFPB moved to revise/replace aspects of the rule amid litigation, so the direction is set, but details are evolving.

6. Enterprise adoption and public sector scale

Usage is no longer just SME-led: consumer adoption has caught up, and public sector use (e.g., tax payments) demonstrates Open Banking’s high-volume, high-trust suitability for critical payment flows.

Leading Open Banking API Examples

Some of the top examples of open banking are given below.

| Open Banking API Provider | Key Features | Supported Regions | Ideal For |

| Plaid | Account aggregation, payment initiation, identity verification | US, Canada, UK, Europe | Fintech startups & neobanks |

| Tink | Payment initiation, personal finance management, risk insights | EU, UK | Banks & large financial institutions |

| TrueLayer | Data APIs, payments, verification | UK, EU, Australia | SaaS platforms & marketplaces |

Open Banking API Challenges and How to Overcome Them

Open banking is rapidly impacting banks globally. This global phenomenon enables banks to increase customer engagement by offering new services and products. Though regulations are driving these changes, there are some market-led modifications that are posing a challenge to the regulators to keep pace with. Let’s explore these challenges.

1. Instability of APIs:

One of the biggest challenges that third-party providers face is the unreliability of payments. Open banking faces issues with its technical infrastructure most of the time. The instability of APIs further creates friction that results in a negative payment experience.

2. Unresponsiveness of APIs:

In June 2025, Open Banking APIs in the UK processed nearly 2 billion calls. Of these, around 10.7 million failed, which translates to a 0.54% failure rate. While this shows substantial improvement in reliability, it still means that server errors, bad formatting, or throttling can impact one in every 200 calls. This continues to be a friction point for third-party developers and users, especially when error messages are unclear or when APIs lack resilience against demand spikes.

3. Lack of standards

To accelerate progress towards a truly open environment, there should be a universally adopted reference model or taxonomy. Right now every bank is crafting its own API with the help of a leading fintech development company that holds expertise in API development and deployment. But, this limits the openness and defeats standardization that holds PSD2 and Open banking together. This creates an issue for the banks to visualize multiple flows.

Next Steps for Banks with Open Banking API

In 2026, the pace of Open Banking adoption is accelerating, driven by evolving regulations, customer demand for real-time services, and the rise of AI-powered fintech solutions. For banks, the challenges, ranging from legacy infrastructure to data utilization, require a proactive, structured approach. The following priorities outline the key next steps for banks to thrive in the Open Banking API era.

| Priority | What It Involves | Why It Matters in 2026 |

| Revamp Legacy Systems | Implement API-first middleware, adopt cloud-native architectures, and enable agile, responsive layers over core banking systems. | Improves integration speed with fintech partners and supports faster product launches. |

| Reinvent the Banking Ecosystem | Build secure, interoperable platforms for 3rd-party providers and embedded finance models. | Expands market reach and meets customer expectations for seamless services. |

| Strengthen Data Management | Apply AI/ML for real-time insights, ensure compliance, and improve data governance. | Enables hyper-personalization and data-driven decision-making. |

| Adopt Comprehensive Business Models | Leverage fintech partnerships, monetize APIs, and explore Banking-as-a-Service opportunities. | Diversifies revenue streams and positions banks as innovation leaders. |

By tackling these priorities, banks can transform from product-centric institutions into platform-based innovators. A robust, agile, and secure Open Banking ecosystem, powered by APIs, microservices, and cloud technologies, will bridge the gap between traditional banking and the open finance future. The result: faster innovation cycles, stronger customer engagement, and long-term competitiveness in a rapidly evolving market.

This ecosystem will definitely bridge the gap between banks and Open Banking APIs by providing a platform for high-speed Open banking requirements. This ecosystem will have next gen capabilities for storage and messaging such as API Development, microservices, cloud, etc.

Still Don’t Have Your Own Open Banking API?

If your bank or fintech hasn’t implemented Open Banking API yet, now is the time. APIs unlock seamless integrations, enhanced customer experiences, and new revenue streams.

Fortunesoft can help you design and deploy robust Open Banking APIs tailored to your business needs, whether it’s account aggregation, payment initiation, or personalized financial services. We ensure your API strategy is secure, scalable, and compliant.

Build Your Open Banking API Today

Conclusion

Open Banking APIs are no longer just a compliance exercise they’re the foundation for a more connected, transparent, and customer-centric financial world. By securely unlocking data, banks and fintech can deliver hyper-personalized products, frictionless payments, and entirely new digital experiences that build trust and loyalty. In 2026, the winners will be those who not only adopt Open Banking but embed it into their core strategy, turning regulation into opportunity and competition into collaboration.

If your customers are already expecting smarter, faster, and more open financial services, the real question is, are you ready to give it to them?